How to Get Out of Foreclosure

This is a simple guide on How to Get out of Foreclosure. There are 7 steps you can take now that can help you get back on your feet and feeling normal again.

Catch up on the mortgage

Pay the mortgage debt in full including all legal fees that the lender incurred. Banks will not accept partial payments after the foreclosure has started.

There are other ways that you can catch up the mortgage without coming out of pocket. You would be selling the house. Contact us for more info about the “subject-to” foreclosure relief option.

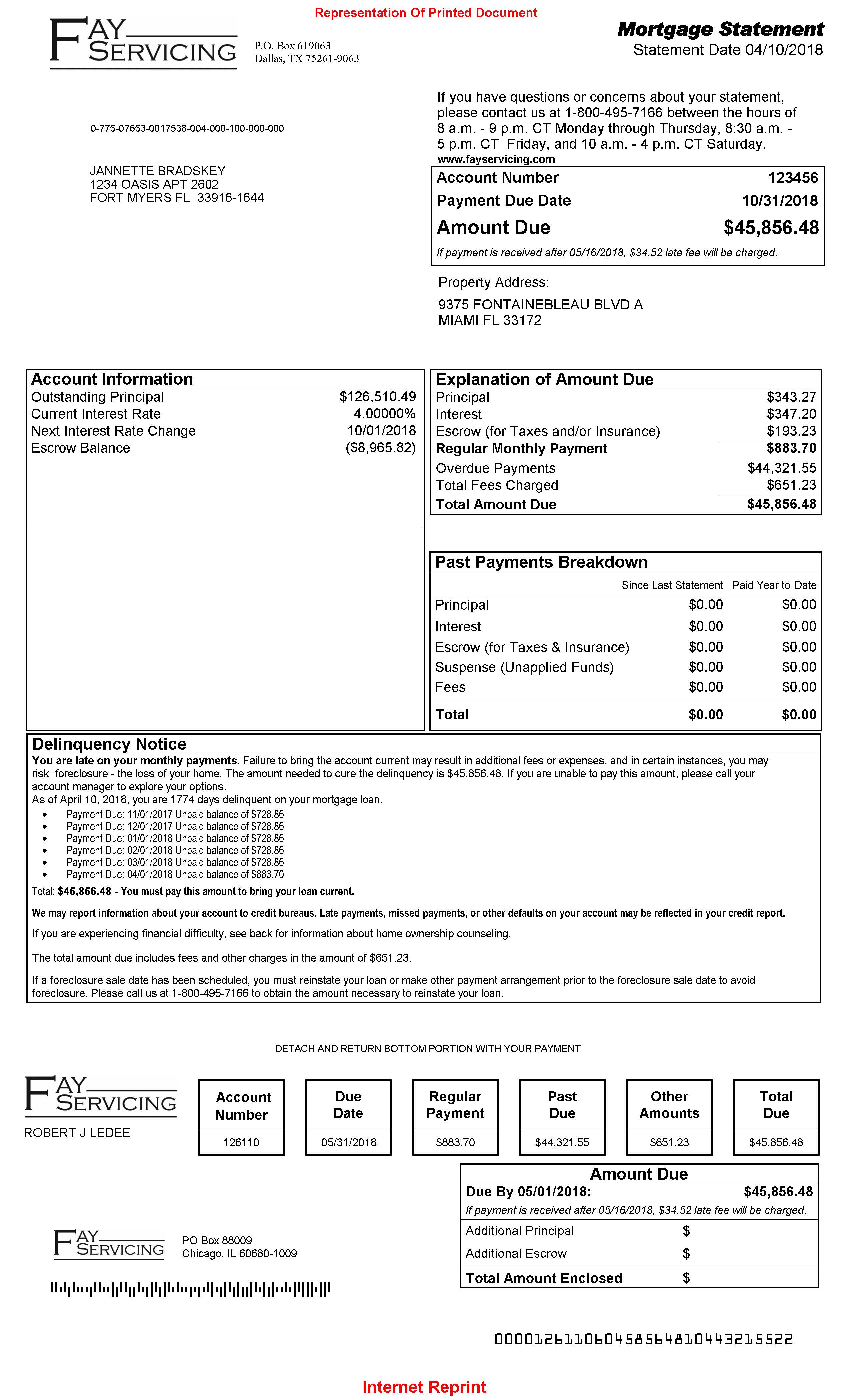

Find out who is your Loan Servicer

Mortgage statement of someone in foreclosure

The servicer is the company servicing the loan for the bank. You can find this by looking at your mortgage statement. You can also find it by looking up your foreclosure case on your local county’s online civil case search system.

Much of your communication will be through them. You want to know who they are in order to get complete and correct documents from them. These documents will be required depending on what exit strategy you decide to take.

Get a Payoff

Mortgage payoff for a short sale

How do you get out of foreclosure if you dont know how much you owe? Call your servicer company and ask for a payoff. The payoff will let you know how much you owe up to that point. this is an important number as it will dictate what your next step is.

Sell it

House in foreclosure short saled by AntlopMIami.com

If you owe less than what your house is worth, you can sell it outright and what’s left of your equity. This is usually the best option considering the benefits and capped long term effects. The biggest obstacle is the emotional attachment to the house. This is one of the best options on how to get out of foreclosure.

Short Sell it

If your payoff is more than what the property is worth, you have negative equity. You can still sell the house through the short sale process. Short sales are free. Click here to find out more about the short sale process.

Find an Attorney

An attorney can help you with a loan modification. You want to make sure you qualify for a loan modification. Click here to see Fannie Mae’s guidelines and see if you qualify.

ALso, make sure not to get hooked into paying $500 or more a moth for the attorney to keep you out of foreclosure. They will only prolong the inevitable and cost you thousands of dollars.

Get a Loan Modification

The lender is going to come out on top. That’s almost inevitable. The bank is betting against you. You want to win, but odds are, if you aren’t careful, you’re going to lose you hat.After all, a loan modification isn’t a refinance. You can refinance when your credit is good and you can afford the loan.

Right now, your credit is BAD. You’ve been missing payments and your score has taken a hit. You’re at their mercy. They will change how they lend you the money in order to “help you get back on your feet.”

Loan modifications are confusing. Partially because of the abundance of legal terms in the documents, it’s easy to agree to something you don’t realize you’re agreeing to.

Loan modifications attract scam artists. A con artist can see when your foreclosure goes into public records. They prey on folks that are in a tight situation and can make decision in haste without knowing what they are doing.

After all, a loan modification isn’t a refinance. You can refinance when your credit is good and you can afford the loan.

Deed in Lieu

A deed in lieu might seem like a good idea on how to get out of foreclosure. The good paty is you are immediately let go of the responsibility. On the other hand, you may experience a very negative impact on your credit. This is as bad a foreclosure. You may still owe the debt and can be at the mercy of the negative impact for years to come.

Foreclosure

Once your house is sold at auction, your house has been foreclosed on. This is the nuclear option and should be avoided along with deed in lieu at all costs. A foreclosure has very negative effects on your credit.

Bankruptcy

Bankruptcy does not get rid of the foreclosure. A bankruptcy gets rid of the amount due so you are no longer responsible. You may qualify for different types of bankruptcies and should talk to an attorney. Selling your home has the same effects of a bankruptcy without your credit being damaged